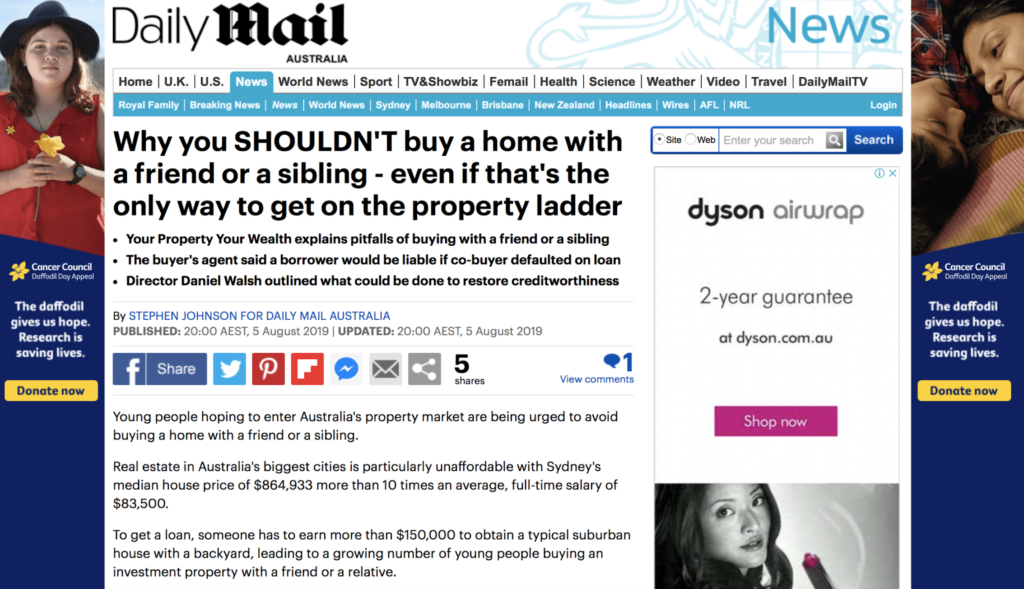

A trend that has become more prevalent over recent years has been co-buying.

What I mean is buying a property with a friend or family member to either live in together or as an investment.

Now, there are a couple of reasons for this, including people generally settling down with a partner later but wanting to get on the property ladder sooner.

Another, of course, is affordability with the power of two incomes making it easier to secure a loan for a potentially better property, too.

There is plenty of guidance around on what needs to be done before buying with someone who isn’t your partner, because while you might be long-term friends or family members, life does tend to change everyone’s goals eventually.

Lending limits

One aspect of co-buying that not many people are discussing, though, is what happens when you want to buy another property independently in the future?

Sure, you might own half a property with your best friend Julie or your brother Josh, but how does that situation impact your borrowing capacity?

Let’s say it’s an investment property that you own with someone else.

Everything has gone quite well for a few years with the rent being split evenly between you as per the terms of the tenants in co-buying common ownership structure.

You use this rent to repay “your share” of the mortgage.

Both parties are quite happy with the arrangement and have no plans to sell up anytime soon.

Over the past few years, you’ve even managed to save some money, too, which you’d like to put towards buying another property by yourself.

So, you head along to your mortgage broker to get the good news about your borrowing capacity.

And that is potentially when the truth of the matter becomes crystal clear.

You see, your broker, let’s call him Jeff, has some info for you that quickly turns your frown upside down.

Jeff tells you that, according to lenders, you are responsible for the entire loan of the property that you bought with Julie or Josh.

Technically it’s called being jointly and severally responsible for the entire loan, he says.

That’s because if your co-owner defaults on their mortgage repayments, the lender will seek to recover the full repayment amount from you.

So, within a few minutes, you’ve learned that you thought you had borrowings of only $300,000 – being half of the loan of the property – but, in fact, lenders will take into account the entire loan amount of $600,000.

On top of that, the bad news continues, lenders will only assign half of the rent to you, which clearly leaves a theoretical big cash flow hole in your finances.

What can be done?

Jeff apologises and says that you’re only likely to be approved for a loan of $200,000, which dashes your dream of buying that post-war renovator on the fringe of a capital city.

You can’t even afford to buy a second-hand unit it seems.

Amongst the myriad bits and pieces that you considered before co-buying, what happened next clearly was not one of them.

One way to remedy the situation would be sell your share of the property to Julie or Josh – if they wanted to buy it.

And another would be to offer buy their share – if they wanted to sell it.

That way you would either have no borrowings and a lump of capital growth cash to your name or you would at least have the full rent included as income in your serviceability calculation, which would hopefully change the goal posts somewhat.

So, as you can see, co-buying comes with a number of pluses and minuses.

The best strategy is always to seek professional advice before journeying down a path that may have a destination that you’d never even considered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}